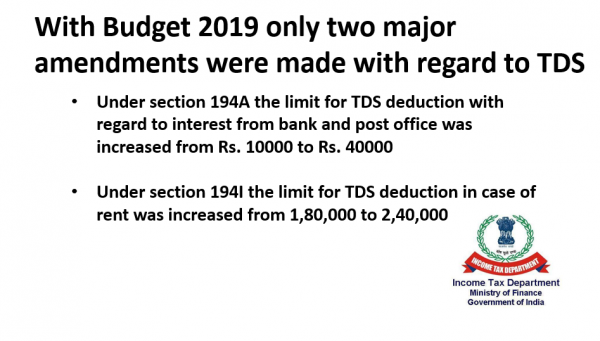

With Budget 2019 only two major amendments were made with regard to TDS:

- Under section 194A the limit for TDS deduction with regard to interest from bank and post office was increased from Rs. 10000 to Rs. 40000.

- TDS rate for section 194DA i.e. Payment in respect of life insurance policy has been increased from 1% to 5%.

- Under section 194I the limit for TDS deduction in case of rent was increased from 1,80,000 to 2,40,000.

Two new section’s have also been introduced:

- New section 194M has been inserted which says, if an individual/ HUF pays to a resident any sum in nature of contract of professional service but such payment is not covered u/s 194C and 194J i.e. payment for personal expense then such individual/ HUF shall deduct TDS @5% if the total amount paid to such resident during an year exceeds Rs. 50 lakh.

- New section 194N has been inserted which says, if any person withdraws in a year Rs. 1 crore from a bank, co-operative society or post office then that bank, co-operative society or post office will have to deduct TDS @2% on amount exceeding 1 crore.

Now let’s take a look at the TDS rate which are most useful:

| Section | Particulars | Limit | Rate of TDS | Applicability for Individual and HUF |

| 192 | TDS on Salary

Deduction needs to be made only at the time of payment and not at the time of credit |

If the taxable income of employee exceeds Rs. 5,00,000/- | At the average rate calculated on his income | Always even if not liable for Audit |

| 194A | Interest other than interest on securities | For bank or post office:

Rs. 50,000 – senior citizen Rs. 40,000 – Other than senior citizen

For other than Bank or post office: Rs. 5,000 |

10% | If the turnover or receipt in previous financial year exceed Rs. 1 crore for business and Rs. 50 lakh for professional even if not liable for audit |

| 194C | Payment to contractor | Rs. 30,000 for single contract

Rs. 1 lakh aggregate amount of all contract paid or credited to one contractor during a financial year |

1% if payment to individual/ HUF

2% payment to others |

If they were liable for Audit under section 44AB of the income tax Act |

| 194H | Commission or brokerage | Rs. 15000 | 5% | If the turnover or receipt in previous financial year exceed Rs. 1 crore for business and Rs. 50 lakh for professional even if not liable for audit |

| 194I | Rent of Plant & machinery or Building and furniture | Rs. 2,40,000 per year | 2% for rent of plant and machinery

10% for rent of building or furniture and fitting |

If the turnover or receipt in previous financial year exceed Rs. 1 crore for business and Rs. 50 lakh for professional even if not liable for audit |

| 194IA | Payment for Purchase of land other than rural agricultural land | Rs. 50,00,00 total consideration* | 1% of total consideration | Applicable without any limit (TDS can be deducted by using PAN number) |

| 194IB | Rent | Rs. 50,000 per month | 5% | Applicable to individual and HUF not liable for Audit (TDS can be deducted by using PAN number) |

| 194IC | TDS on JDA agreement | No Limit

TDS will be deducted when consideration is not in kind |

10% | |

| 194J | Payment for Professional, Technical fess or Royalty fees | Rs. 30,000 per year | 10%

2% in case the payee is call centre |

If the turnover or receipt in previous financial year exceed Rs. 1 crore for business and Rs. 50 lakh for professional even if not liable for audit |

| 194M | Payment for any contract or professional fees other than those covered under 194C and 194J | Total amount paid during a year exceeds Rs. 50 lakh | 5% | Applicable even if not liable for audit and paid for personal expense |

*Total consideration will include any amount paid in name of membership fee, car parking fee, maintenance fee or advance which is incidental to transfer of property.

Provided that no deduction shall be made u/s 194C or 194J if payment is made for personal purpose i.e. paying to contractor for constructing residential house or paying professional fees to doctor for personal health etc.

If you need assistance you can ask a question to our expert and get the answer within an hour or post a comment about your views on the post.

{kind=link}